Priced Out of Calgary? How a Basement Suite Increases Your Mortgage Approval

The Direct Answer

If you've been told you're priced out of buying a home in Calgary, here's something worth knowing. A home with a legal basement suite can help you qualify for a much bigger mortgage. Lenders can count up to 100% of the rent from a legal, self-contained suite as part of your income. You usually need to live in the home yourself, and the suite has to meet a few requirements. But the bottom line is simple: the bank treats your future tenant's rent like it's part of your paycheck.

This is the idea behind the "mortgage helper" strategy. It's one of the most useful tools out there for Calgary buyers who think homeownership is out of reach, and most people don't even know it exists.

The CMHC Rental Income Rule

When a lender decides how big a mortgage you can get, they look at two numbers: your Gross Debt Service (GDS) ratio and your Total Debt Service (TDS) ratio. Both of these compare your housing costs and other debts against your income. The more income you can show, the bigger mortgage you can qualify for.

If you own the home and live in it, and it has a legal secondary suite, lenders can count a big chunk of that rent toward your income. Some lenders count up to 100%. Others count less. It depends on the lender. But the basic idea holds true almost everywhere: a legal, self-contained suite with its own entrance, in a home you live in, can boost how much mortgage you qualify for. The suite usually needs a track record of rent coming in, or for a brand-new suite, an appraisal showing what it could rent for. It also has to follow local zoning and building rules.

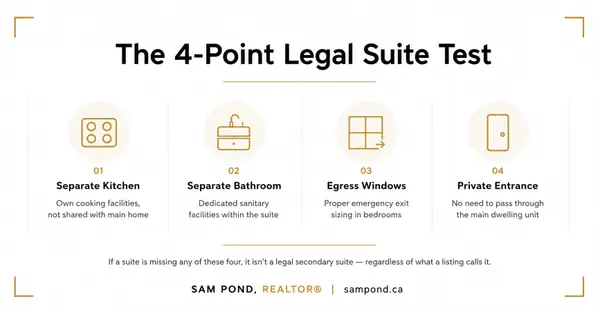

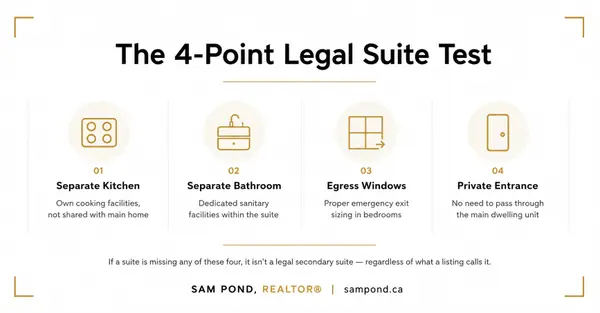

This is why "legal" matters so much. If the suite isn't legal, the bank usually won't count the rent at all, no matter how much it could actually bring in. I've written about the difference in detail already: Legal Secondary Suites in Calgary: What Buyers Need to Know covers what actually qualifies as legal, and Illegal Secondary Suites in Calgary: What Buyers Need to Know covers the tradeoffs if you're weighing an unregistered one instead. For now, just know this: legality is the key that unlocks this whole strategy.

Example: Salary Alone vs. Salary Plus Rent

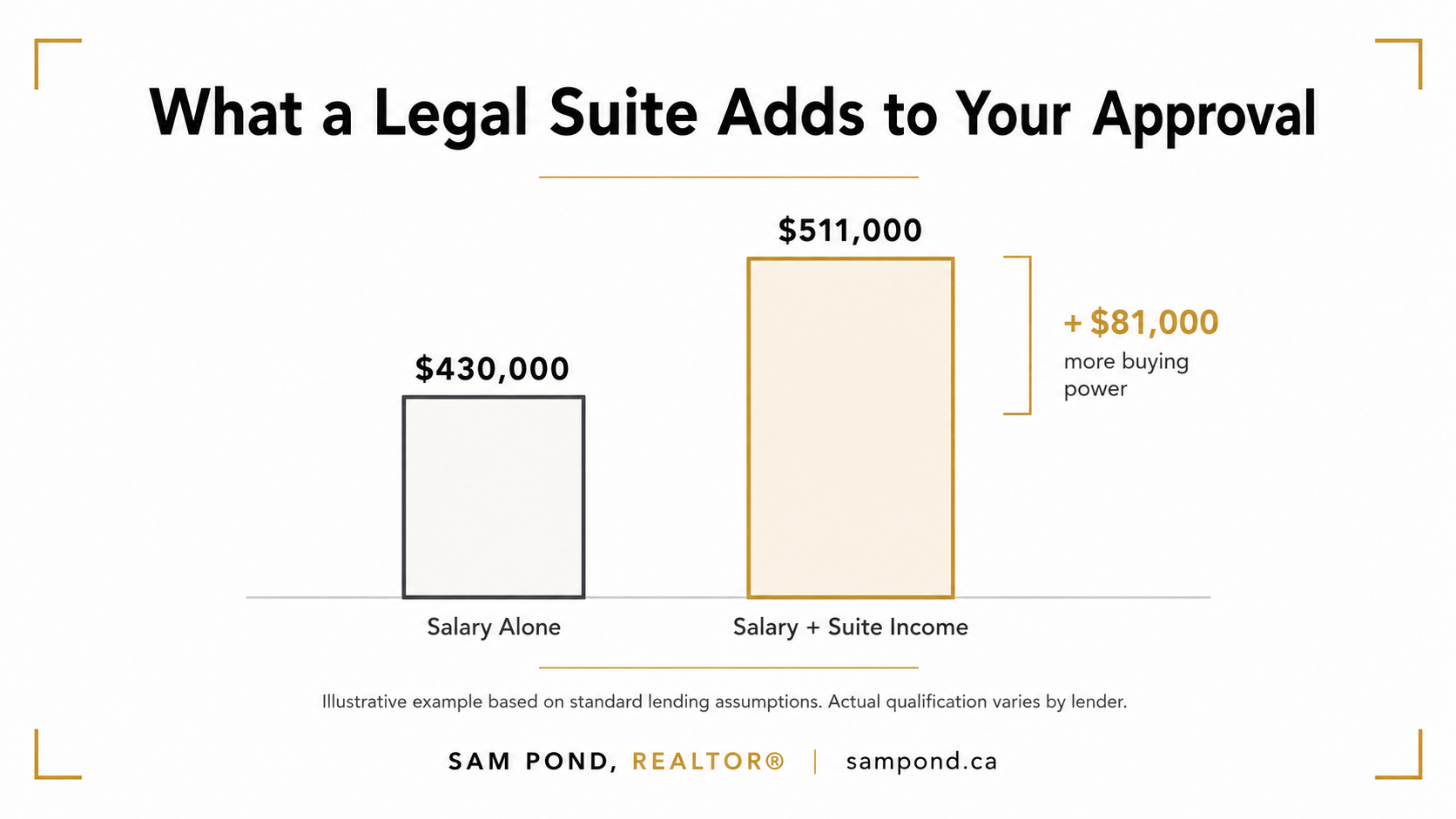

Let's make this real with an example. (These numbers use standard lending assumptions to show how the math shifts. Your actual numbers will depend on your income, your debts, your lender, and the suite's rent history.)

Scenario A, salary alone: A buyer earning $90,000 a year, with no rental income to add, qualifies for a mortgage of roughly $430,000 based on their paycheck and a typical amount of existing debt. In a city like Calgary, that often means looking at smaller condos or homes further from the core.

Scenario B, salary plus suite income: Same buyer, same $90,000 salary. But this time they're looking at a similar home that happens to have a legal basement suite renting for $1,250 a month. Once that rent gets added to their income at 100%, their mortgage ceiling jumps to roughly $511,000. That's about $81,000 more in buying power, just from one tenant's rent.

That gap between Scenario A and Scenario B is the whole point of this strategy. It's not a trick or a loophole. It's a normal, well-known way that lenders underwrite mortgages. Most first-time buyers just don't know about it yet.

This Isn't Hypothetical

I saw this play out with a client not long ago. Some of you have already read about him, he's the buyer I mentioned in my posts on legal and illegal secondary suites, the one who started out on a home with an illegal suite and walked away after the inspection made the risk real instead of theoretical.

Here's the part I hadn't shared yet. When he was looking at that first home with the illegal suite, his purchase price limit was $700,000, because the suite's rental income couldn't be counted toward his mortgage application at all. Once he shifted his search to a home with a legal suite, his budget increased by $50,000, up to $750,000, simply because the bank could now count that suite's income as part of his application. Same buyer, same income, same debts. The only thing that changed was whether the suite was legal.

That's not an illustrative example with disclaimers attached. That's what actually happened.

Why Parents Are Encouraging This Strategy

Here's something else happening across Calgary right now. Parents who've owned a home for twenty or thirty years are pushing their adult kids toward suited properties as their first home, instead of a smaller place with no suite.

These parents have watched their own home become the biggest part of their net worth. So when they're in a position to help their kid buy a first home, a lot of them want that help to go toward a property that pays for part of itself. It's not just about handing over money for a down payment. It's about putting that money into something that builds equity faster, with a tenant covering part of the cost every month.

This "Bank of Mom and Dad" support isn't just generosity. It's parents realizing that a suited home is a different kind of investment than a regular starter home. It pays part of its own mortgage. It builds equity for their kid. And it makes the whole idea of helping financially feel a lot less risky.

What This Means for You

If you've been told Calgary is out of reach for you, the math might be telling a different story. A legal basement suite can change your qualifying amount by tens of thousands of dollars, and a lot of buyers, and even some agents, don't think about it early enough in the search. Before you write off a neighborhood or a type of home, it's worth running your actual numbers with a mortgage professional to see what a suited property could really do for your approval.

If you're thinking about this strategy for yourself, or trying to figure out how to help your own child buy their first home this way, I'd be glad to walk through what that could look like for you.

A Few Honest Questions People Ask

Does the suite have to be legal for the rent to count? Yes. If the suite isn't registered with the city, most lenders won't count the rental income at all, no matter what it could actually bring in. Legal Secondary Suites in Calgary: What Buyers Need to Know covers what actually qualifies.

Do I have to live in the home to use this strategy? Generally yes. This approach applies to owner-occupied properties, meaning you live in the main home and rent out the suite, not a property you're buying purely as a rental.

What if the suite doesn't have a tenant yet? Lenders can often use an appraisal showing what the suite could reasonably rent for, instead of an existing lease. The exact requirements vary by lender.

Does every lender count 100% of the rent? No. Some count up to 100%, others count less, and the calculation method (adding the rent to your income versus offsetting your housing costs) also varies. This is exactly the kind of thing worth confirming with a mortgage professional before you count on a specific number.

Browse homes that already have a legal secondary suite: Single Family Homes With Legal Secondary Suites.

This article is for general education. It isn't mortgage, legal, or property management advice. The example numbers above use standard lending assumptions (a 5.25% qualifying rate, 25-year amortization, and typical property tax and existing debt levels) and are for illustration only. Your actual qualifying amount will depend on your specific income, debts, credit, and lender. Mortgage rules vary by lender and change over time. Always confirm the current details with a licensed mortgage professional before making decisions.

Recent Posts